By Eddah Waithaka

Diamond Trust Bank (DTB) has projected a significant increase in lending to individuals and small businesses, citing Kenya’s stabilizing economy and steady growth following a challenging year.

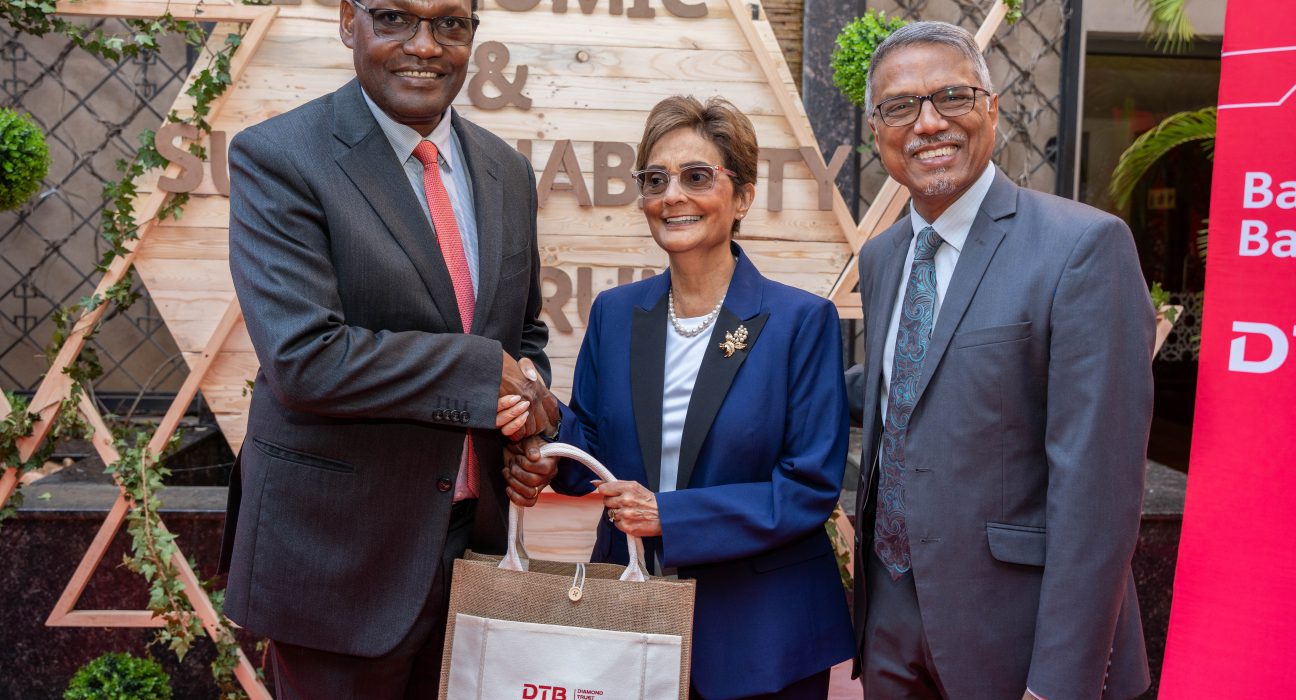

DTB Kenya Chief Executive Officer Murali Natarajan announced that the banking sector’s credit could double in the next decade from the current $32 billion if the current economic momentum is sustained.

Speaking at the DTB Economic and Sustainability Forum in Nairobi, Natarajan emphasized that the immediate beneficiaries of this growth will be individuals and small businesses.

“When I look at the resilience of the economy and the track record of having dealt with so many challenges, that gives me immense confidence about the future,” he said.

Natarajan highlighted the untapped potential in the Micro, Small, and Medium Enterprises (MSME) sector, which includes both formal and informal businesses. “As banks start focusing on retail and SMEs, I see a big opportunity there. By focusing on segments like agriculture, retail, and MSMEs, and making our offerings more accessible, we should be able to double our balance sheet in about three to four years,” he added.

To achieve this, DTB plans to expand its digital offerings, forge strategic partnerships, and increase its branch network to reach more customers. Natarajan attributed his optimistic forecast to Kenya’s economic stability, driven by lower interest rates, favorable weather conditions, and reduced fuel prices.

Read More On: https://africawatchnews.co.ke/nba-africa-and-safaricom-launch-m-pesa-jr-nba-to-inspire-young-athletes-across-east-africa/

He also commended the government and the Central Bank of Kenya for navigating the economy through last year’s difficulties. “The macros look stable, interest rates are coming down, and remittances from Kenyans abroad continue to flow,” he noted. DTB projects Kenya’s economic growth to reach 5% this year, though challenges and risks remain.

Dr. Chris Kiptoo, Principal Secretary for the National Treasury, echoed this optimism, stating that the worst of the economic difficulties is behind the country. “When I started, it was very hard, and I had many sleepless nights. Now the worst is over, and the future is brighter. We have a resilient and diversified economy, which helps us recover from shocks,” he said.

Dr. Kiptoo outlined the government’s priorities for the next financial year, focusing on agriculture, exports of tea, edible oil, cotton, leather, dairy, natural resources, building materials, and the blue economy.

To further boost private sector lending, he announced plans to transfer the Credit Guarantee Scheme to a government-owned company to ensure its continuity.

The scheme, currently an arrangement between the government and seven banks, commits the government to cover a portion of outstanding amounts in case of default.

Additionally, Dr. Kiptoo revealed that the committee verifying pending bills has approved the payout of KSh236 billion out of the more than KSh600 billion inherited by the Kenya Kwanza administration. The bulk of these funds will go to small businesses and road contractors, providing much-needed relief to these sectors.

The government will also prioritize implementing the Single Treasury Account, e-procurement policy, zero-based budgeting, and Public-Private Partnerships (PPPs) to increase development spending and enhance economic stability. Kenya will remain in the International Monetary Fund (IMF) program to maintain fiscal discipline and support recovery efforts.

As DTB and other financial institutions gear up to capitalize on the improving economic climate, individuals and small businesses are poised to benefit from increased access to credit, driving growth and innovation across the country.

Read More Stories On: https://africawatchnews.co.ke/